infrastructure

James Stewart: Can We Afford to Pay for the World’s Infrastructure Needs? We Can’t Afford Not To

Paying the word’s infrastructure needs is daunting, which is why we need real leadership and innovative thinking.

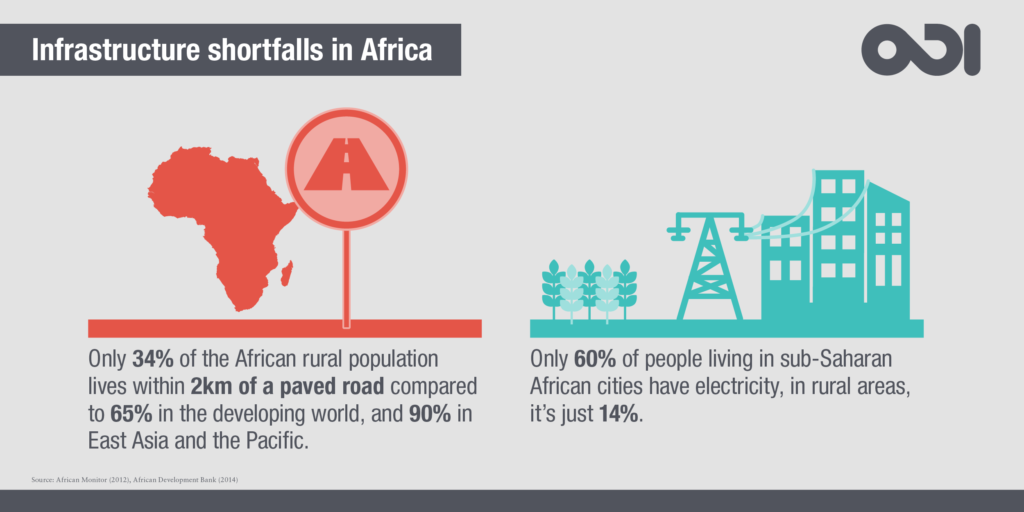

Unfathomably big numbers can be exhausting. When it comes to infrastructure, there’s significant gap between ambition and reality, as the Overseas Development Institute (ODI) in London has illustrated in a series of infographics. The world is facing unprecedented demand for infrastructure investment through 2030: $57 trillion globally, $16 trillion in Europe, $8.1 trillion in North America, $9 trillion in Asia, $1.8 trillion in Sub-Saharan Africa and so on. These numbers certainly set a stage for discussion, but delivering action on that requirement will take partnership and a lot of hard work from a broad spectrum of public and private participants.

The first and perhaps biggest challenge is to find the means to pay for all of this infrastructure. The current fiscal squeeze happening all over the world means less funding from direct taxation off the balance sheets of governments and more use of alternative funding sources such as user charges, value capture revenues and local hypothecated taxes. All in all, these new types of cashflow are a much riskier proposition for any financier than direct government-sourced funding.

Combine this with a reduction of capacity in commercial lending markets and a lower risk appetite as a result of the global financial crisis, and financing infrastructure has become a lot more complicated in developed markets — let alone developing and low-income countries. The good news is that deals are still being financed, and from an ever broader range of debt providers. Traditional project finance banks are still lending most of the money, but institutional investors like Allianz are emerging fast.

However, it is easy to be fooled. The fact is that the current pipeline of deals is way below what is needed to actually address those really big numbers. For example, the Tappan Zee Bridge Replacement is a mega project in the United States and expected to cost around $4 billion. In order to invest the nearly US$60 trillion in projected global need, we need to develop roughly 15,000 mega projects of equal size to Tappan Zee in the next 15 years — or roughly 1,000 $4 billion projects every year. If investment levels are to increase to achieve the targets that governments need and want, there will not be nearly enough global financing capacity – particularly in the developing markets.

At the heart of the solution to this problem is the development of a sustainable, long-term financing market. That means bringing in a large pool of institutional debt providers like pension funds, sovereign wealth funds and insurance companies rather than relying solely on the constrained capacity and shorter tenors of the traditional commercial banking market. This is fine in theory, but on most projects there is risk gap that needs to be covered before the institutions will lend.

The good news is that action is being taken to address this problem. Governments, development banks and multilaterals have realised that they cannot simply go it alone and lend directly to projects to alleviate the problem. They do not have the balance sheet capacity for the trillions of dollars of investment required. Therefore the big shift in policy has been the recognition that these institutions need to leverage their capital, cover the risk gap and help bring in private-sector debt capital.

What we are now seeing is the introduction of new credit-enhancement facilities designed to lift the project’s risk profile to an acceptable level for institutional debt — either through guarantees as we’ve seen in the United Kingdom, or first-loss mezzanine capital from institutions like the European Investment Bank and Asian Development Bank. The other positive development is a significant increase in the amount of capital available through new multilateral vehicles like the $100 billion China-led Asian Infrastructure Investment Bank.

Courtesy of ODI.

Courtesy of ODI.These are all excellent initiatives, but it is all happening far too slowly. Mega projects frequently take a decade or more to develop and construct. We have 15 years to deliver tens of thousands of projects. There is a real danger that governments and multilaterals are trying to be too clever with these new credit-enhancement facilities and simply not recognizing the wider picture — that what this is really about is accelerating the development of new infrastructure, which is going to create jobs and foster economic growth. This will in turn alleviate poverty and address social issues.

For the private sector, infrastructure is really just another deal. They will go at their own pace dictated by their own commercial considerations. For governments and their citizens — infrastructure is their livelihood. They are the main beneficiaries both in economic and social terms as they try to manage growing populations, urbanisation and ever-greater demand for basic services.

Governments and communities cannot afford further delays. Governments at all levels need to intervene more and recognize their role in making the market. This may require them to take more risk and pay a bit more in the early years, but it can be justified in terms of the long benefits being generated. Once the market is established governments can step back, but we need leadership and action right now.

(Top image: Courtesy of Shutterstock)

James Stewart is Chairman of KPMG’s Global Infrastructure practice.

James Stewart is Chairman of KPMG’s Global Infrastructure practice. All views expressed are those of the author.