investors

Investor Update: Recent IR Events And Your Questions Answered

I hope this note finds you and your family healthy and well. Over the past two weeks, GE has participated in several investor events and meetings, and has continued to take liquidity-enhancing, leverage-neutral debt actions like you saw on Monday. I thought it might be helpful to summarize them in one place for you as well as provide answers to some of the more commonly asked investor questions during that timeframe.

On May 28, our CEO Larry Culp presented at the Bernstein Strategic Decisions conference and participated in a fireside chat where he answered questions from investors. During the event, Larry reiterated our near term focus on safety, serving customers, and preserving our financial strength, and also provided an update on our end markets, business operations and actions we are taking to mitigate the impact of COVID-19. You can find a replay of the event here.

On June 3, our Gas Power CEO Scott Strazik presented at the UBS Industrials and Transportation Conference and also participated in a fireside chat. Scott described the efforts that the team is making in its multi-year turnaround, some early but encouraging signs of progress, and the path to high single digit operating profit margins and positive free cash flow* in 2021. You can find a replay of the event here. In addition, GE Healthcare CEO Kieran Murphy met with a group of investors on June 4, and the slides he used during the discussion are available here.

During and following these events, we have also received feedback and questions from a number of you primarily related to the impact of COVID-19 on our operations, cash flow, and financial position, and especially with regard to what we’re seeing in Aviation, GECAS and Healthcare. Consistent with past practice, I thought it would be helpful to use this newsletter to capture and address the most frequently asked questions over recent weeks. As we continue to remind investors, the current environment poses numerous challenges to GE, but we’re taking swift actions on cost and cash that are helping to accelerate our multi-year transformation.

Thank you for your continued interest in GE, and please stay safe.

Steve

_________________________________________________________________________________

1. GE recently mentioned that Industrial free cash flow* would be negative in 2020. What gives you confidence that you can achieve positive free cash flow* in 2021 and high single digit free cash flow margins* over time?

GE has confidence in the Industrial free cash flow* targets described at the Bernstein Strategic Decisions Conference because of the initial signs of improvement that we see in our end markets, the actions we are taking to reduce cost and preserve cash, and the lean transformation that is taking hold across the company.

As Larry discussed at the recent Bernstein Strategic Decisions Conference, all of our GE businesses have been negatively impacted by COVID-19, especially Aviation, GECAS and Healthcare. While uncertainty around the pace of recovery in our end markets remains, we are watching key leading indicators closely, are focused on things that we can control, and should achieve positive free cash flow* in 2021 given what we see today on our journey toward high-single-digit free cash flow* margins over time.

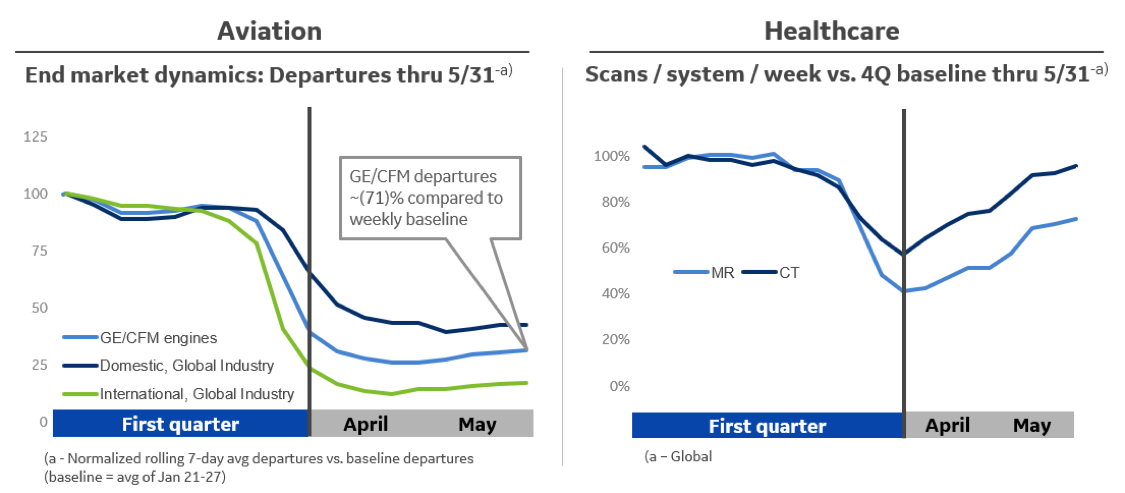

Although the shape of the recovery is still unknown, we have started to see some positive market data trends across our portfolio. In Aviation and GECAS, aircraft departures, which are a leading indicator for billings and revenue generating shop visits, are improving in China (now down ~30% versus ~70-80% at the beginning of 2020) and freight is up, which is especially meaningful as 30% of our widebody engines are cargo-related. Global departures as of May 31 were down 71% and have since improved to down 67% as I write this today. In Healthcare, we are starting to see a recovery in the number of scans being performed on our CT and MR machines which tells us that demand for our non-COVID specific, higher margin products like Pharmaceutical Diagnostics should start to recover in the second half. Neither of these two examples are reasons to celebrate today, but we are encouraged by what appears to have been a bottoming at this point in time and a turn in the right direction.

Based on our market realities as we see them today, we do expect Industrial free cash flow* to be negative in 2020 (with the second quarter between $(3.5) billion - $(4.5) billion). Given that reality, we’ve been especially focused and moving quickly to take more than $2 billion of cost cutting and $3 billion of cash preservation actions, 80% of which should come through in the second half of 2020. These actions include permanent and temporary workforce reductions, discretionary spend cuts, capital expenditure reductions, and working capital improvements. Looking forward, so far one-third to one-half of these cost and cash actions should be permanent in nature, but there is a lot in motion, and we are working to increase this over time which will help on a more sustained basis into 2021.

Driving cost out is important of course, but this pandemic is providing the opportunity, painful as it certainly is, to accelerate GE’s transformation beyond just cost actions so that when we do see those long-term trends that benefit our businesses reemerge, we'll be well positioned to return to profitable, cash generative growth. Our teams are doubling down on lean, adopting digital technologies faster, and innovating to serve new customer needs—which all serve to make us more nimble, more customer-centric and ultimately more effective on the other side of this pandemic.

While our FCF margin has taken a step back this year as a function of COVID-19, we expect to emerge post the pandemic not only with a better, more competitive cost structure but with stronger franchises that are implementing lean to continuously improve operations and in turn improve working capital efficiency and expand margins that fall through to cash. Aviation and Healthcare continue to be well positioned in long term structurally attractive markets, and lean efforts along with cost and cash actions across each should bear fruit. And in our Power and Renewables businesses, we continue to focus on right sizing our cost structure to market realities and running off inheritance cash items and legacy projects. Coupling the execution of these priorities with our fundamental strengths in technology, team, and global reach gives us high confidence that we will reach high single digit free cash flow margins over time.

_________________________________________________________________________________

2. It sounds like your Aviation business has been most impacted by COVID-19, which was the largest generator of earnings and free cash flow* for GE in 2019. How should we think about the pace of recovery in 2020/2021+ and what are you doing today to help mitigate the impact?

The recovery of our commercial Aviation business will depend on the pace at which commercial air traffic resumes and the rate at which airframers produce new aircraft. We expect the recovery to be supported by continued strong demand in our Military business, the cost & cash actions we are taking across the business, and the underlying strength of our technology, customer relationships, and installed base.

Our Aviation business has been hit hard and fast by COVID-19 as evidenced by the recent dramatic decline in commercial air travel which, at its worst in April, was 76% below a pre-COVID-19 baseline. Despite these current headwinds and the uncertainty surrounding the shape of a market recovery, we believe that our Aviation business is well positioned to manage through this pandemic and emerge stronger on the other side for several reasons.

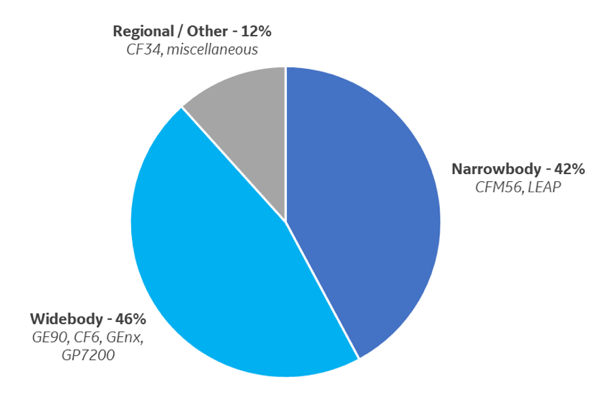

Not surprisingly, our commercial services business ($15.2B of revenue in 2019) has experienced the greatest impact as airline customers take actions to conserve cash such as parking aircraft while demand remains low or delaying engine maintenance until those engines are needed again. We also expect these market dynamics will lead to hundreds of millions of dollars of charges related to our long-term service agreements. However, we along with many others in the Aerospace industry expect that domestic travel routes primarily served by narrowbody aircraft will recover before international travel routes which are primarily served by widebody aircraft. In GE Aviation’s case, more than 40% of commercial aftermarket revenues and profits come from the CFM56 and LEAP narrowbody engines produced by our CFM International joint venture, while GE’s widebody engines such as the GEnx, GE90, and CF6 provide operational cost benefits and/or alternative applications to commercial passenger travel (e.g. freight). In any case, the pace of recovery in this part of the business will primarily be dependent on customer confidence in air travel and a subsequent increase in commercial departures. You can see more detail on our 2019 commercial services revenue below.

2019 Commercial Services Revenue by Aircraft Type

We have also seen some of our customers announce fleet retirements, and we expect that we will see more depending on the pace of recovery in the industry and other factors such as oil prices. As aircraft retire, operators often harvest and resell used parts from their engines (used serviceable material, or USM). Understandably, some worry that an influx of USM into the aftermarket will in turn have a negative demand impact for GE’s new spare parts.

In addition to the fact that GE is positioned with a younger vintage fleet relative to other engine manufacturers and also a significant presence in cargo applications, three dynamics are at play when considering an influx of used material from an increase in retirements: the condition, hardware configuration and our experience with USM.

- First, as an example of condition, consider that just under 30% of CFM56 engines are flown in hot and harsh environments. Engines that operate in hot and harsh environments translate to fewer high value spare parts available for re-use as compared to an engine that was not flown in a hot and harsh environment. Additionally, maintenance providers typically require parts from engines that were not flown in a hot and harsh environment, so we anticipate less USM coming into the market as a result.

- Second, with regard to hardware configuration, GE and CFM invest in upgrades that improve our customers’ fuel burn and time on wing. This has two important effects. One, because our customers can fly these aircraft longer and more efficiently, they are less likely to be retired early when compared to the same aircraft model powered by competitors’ engines. And two, as a function of the upgrades, older part models harvested from older fleets that do retire cannot be used on newer engines.

- Finally, our team has over 20 years of experience in buying, selling, and using USM, including using USM within our CSA contracts. While increased USM in the market still poses a risk to new spare part sales, we also benefit from lower costs when we utilize USM where it makes sense to do so for our customers.

Our commercial engines business ($9.0B of revenue in 2019) produces installed and spare engines for both Airbus and Boeing. Revenue in this part of the business generally follows aircraft production rates at each, which for the time being have been reduced as a result of COVID-19. Going forward, we are in close contact with our airframer customers to ensure our supply chain operations are sized appropriately for production today and are ready when production picks back up in the future. We have spent more than a decade refreshing key programs in our commercial engine portfolio with investments in the GEnx, LEAP, and GE9X engines, and are well positioned with airframers and our airline customers to grow this part of the business as demand for new aircraft returns over time.

We continue to see strong demand for our Military products ($4.4B of revenue in 2019) as we deliver new equipment and spare parts to our Armed Forces. We are also ramping up several customer funded engine development efforts (e.g. the T901 helicopter engine) and advanced science & technology programs which have allowed us to shift some of our engineering resources from the Commercial business to Military.

In order to mitigate the impact of COVID-19, GE Aviation has announced more than $1 billion of cost actions and more than $2 billion of cash actions that will impact 2020, primarily in the 2nd half of the year. We expect that these actions will help improve decremental margins through the year and, in line with our estimate for the company, one-third to one-half of these actions should be permanent – a number we are working to increase over time. These actions, including a ~25% reduction in Aviation’s total workforce, are not being taken lightly but are necessary in order address our current reality head on while still maintaining our core strengths and flexibility to deliver for our customers in the future.

Finally, the GE Aviation franchise is one built on leading technology, strong customer relationships, and a large installed base. These are strengths that don’t fade in the face of a pandemic, and in many cases help GE and our customers be successful during downturns. Our teams are rising to the challenge of COVID-19, and we’re confident that GE Aviation will be a better business on the other side.

_________________________________________________________________________________

3. Can you explain how the CFM joint venture (JV) between GE and Safran works in the aftermarket, operationally and financially?

The 50/50 CFM joint venture with Safran is an important partnership for GE Aviation. GE and Safran each have responsibility for different parts of CFM and LEAP engines and recognize aftermarket revenue based on the spare parts, part repairs, and overhauls that each entity sells or performs.

The CFM joint venture was created in 1974 as a means to combine GE’s and Safran’s aerospace expertise and technology, to share risk, and to create cost efficiencies in the collaborative development of the CFM56 and LEAP engines. These engines are now used on multiple narrowbody platforms including several generations of the Airbus A320 and the Boeing 737. As part of this JV, both GE and Safran are responsible for the development and production of separate modules of the engine for both new engine production and spare parts fulfillment (and the associated costs).

While the equity ownership in the JV is split 50-50 between GE and Safran, there are several reasons why the total CFM related aftermarket revenue and profit recognized by each entity will differ. First, GE does not consolidate the CFM JV revenues into its financials. Rather, the revenues that are presented in GE’s commercial aftermarket revenues are reflective of the actual spare parts, part repairs, and engine overhauls sold and performed.

On spare parts, GE is the manufacturer for the compressor and high pressure turbine on both CFM56 and LEAP engines, and those engine parts are more frequently replaced at the time of service. Therefore, GE has historically recorded aftermarket spare part revenues that are greater than 50% of the total aftermarket parts sales for CFM56 and LEAP engines. For example, while it will fluctuate based on the mix of shop visits, GE’s 2019 share of new CFM56 spare part sales recorded in the two CFM JV entities (CFM International Inc. and CFM International SA) was more than 60% of total CFM56 new spare part sales. It’s worth noting that GE’s CFM56 services revenue includes 100% of shop visit revenue where GE completes the overhaul (CSA and Time & Material) while revenue related to external shop visits performed by MROs other than GE only includes revenue from part sales and part repairs.

On part repairs and engine overhauls, GE and Safran each independently perform this work at their respective service facilities and the associated revenues generally run outside of the CFM JV. GE has a large network of part repair and overhaul facilities and has historically conducted more CFM engine overhauls in GE shops than Safran does in their shops.

The combination of these three factors (spare part mix, part repair revenues, and engine overhaul revenues) are the main reasons that commonly result in GE recognizing higher CFM56 revenues than Safran.

_________________________________________________________________________________

4. How does your GECAS valuation process work and should we expect large asset impairments in that business this year?

GECAS continually monitors its portfolio throughout the year, including the current 2nd quarter, and performs its annual valuation review in the 3rd quarter. This valuation review is based upon both estimated future cash flows of each aircraft and independent third party appraisals. Based on what we see today, we expect to see some level of elevated impairments in 2020.

We continually monitor our GECAS portfolio throughout the year, including the current 2nd quarter, and will perform additional customer specific reviews if a contract specific trigger occurs at any point throughout the year (e.g. an asset repossession). In the 3rd quarter of every year, the GECAS team completes a rigorous annual valuation review to determine if the estimated fair value of each commercial aircraft in the GECAS portfolio is above the value on GE’s books. As part of this process, the GECAS team estimates the cash flows remaining over the entire estimated life of each individual aircraft (not just the next year or two) which includes current contractual lease information along with estimates for variables such as future lease rates, lease periods, and redeployment costs (it is important to remember that these are long lived assets (25+ years) that we expect will continue to be leased well beyond the current downturn). The GECAS team then incorporates independent third party appraisals to establish fair market values for each asset and determine if an impairment is required.

Based on what we have seen to date with our customers and our view of the market going forward, we do anticipate pressure on our cash flow assumptions and therefore some elevated level of impairments during this year’s annual review. While every downturn is different, elevated impairments are consistent with what we have seen in previous downturns such as 9/11 and the Great Financial crisis when after-tax impairments averaged roughly ~$200 to ~$400 million per year for each of the following two years. Based on what we see today, we expect to see some level of elevated impairments in 2020.

While this has certainly been a challenging time for GECAS, our portfolio today is better positioned than in previous downturns to manage through to the other side of COVID-19. For example, more than 85% of our commercial aircraft portfolio are Tier 1 or 2 assets (considered the most attractive narrowbody and widebody aircraft) and 60% of our fixed wing portfolio is narrowbody aircraft which we expect to recover faster than other aircraft types. Our experienced leadership team is working with our customers every day to understand their long-term liquidity and fleet needs, and we believe that aircraft leasing will continue to be an attractive financing option for airlines going forward.

_________________________________________________________________________________

5. Has your approach to strengthening your balance sheet changed in light of the current environment, and how are you thinking about what’s next?

We are focused on keeping our financial position strong and safe with a keen eye on cash flow and capital discipline, leverage, and liquidity amid this uncertain environment. Looking forward, we continue to monitor our operations in this environment, prioritizing maintaining a high level of cash and maximizing our flexibility as we evaluate any next steps.

Strengthening our balance sheet is still a top priority, all the more so in light of the uncertainty created by COVID-19. We have worked hard to put GE on firmer financial footing and have made progress. First, the cost and cash actions, operational rigor, and process improvement we discussed earlier will all serve over time to help us improve our cost structure and deliver more sustainable performance and cash flow generation in our businesses.

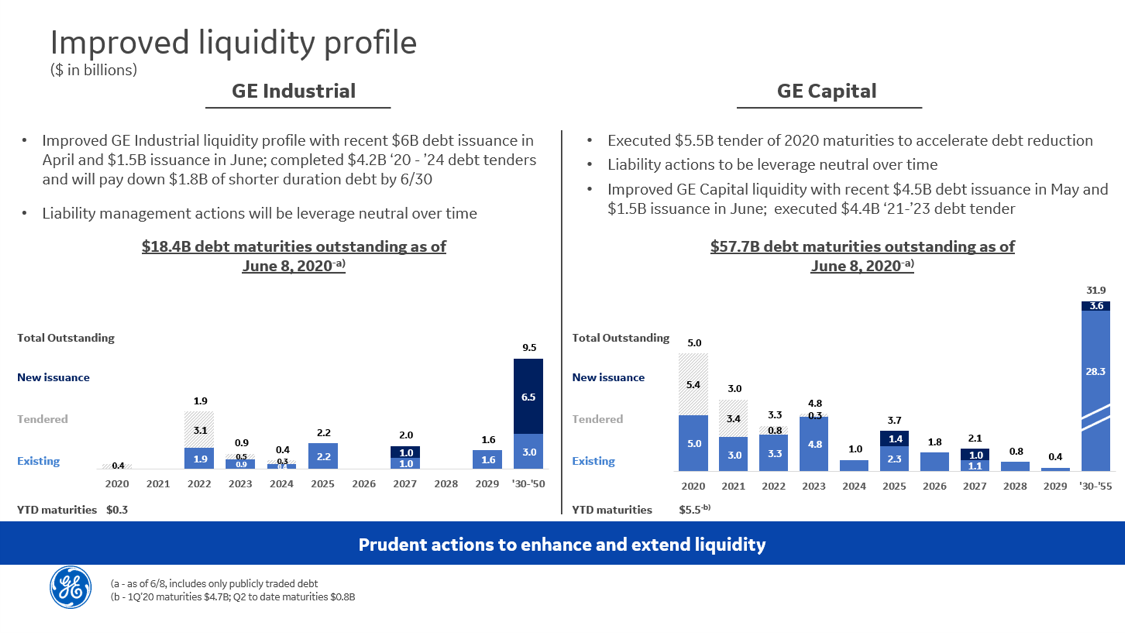

Second, we’ve continued our efforts to reduce debt in 2020, including reducing Industrial debt by ~$8 billion and reducing Capital debt by ~$4.9 billion so far this year.

Third, we’ve taken several steps to prudently manage our liquidity and risk profiles. As of March 31, 2020, GE held cash, cash equivalents, and restricted cash of more than $47 billion, including ~$34 billion in Industrial & more than $13 billion in Capital. The net proceeds of $20 billion that we received from the BioPharma transaction have given us more flexibility to de-risk and further strengthen our balance sheet. And, as part of our planned financial management process, we refinanced our existing revolving syndicated credit facility, extending access to $15 billion in liquidity through 2023.

In April and May, we also took a series of leverage-neutral actions to enhance our near-term liquidity at both GE and GE Capital, issuing $6.0 billion at GE and $4.5 billion at GE Capital of longer-dated debt and tendering for shorter-dated debt to extend ~$4.2 billion of GE maturities and ~$4.4 billion of GE Capital maturities so far. As a result of these actions, we now have $5 billion of GE Capital long-term debt maturities in 2020 and $3 billion in 2021, with no remaining GE maturities scheduled over that same time frame.

Using excess proceeds from the Industrial debt offering, we’re targeting repaying $1.8 billion of debt and commercial paper by the end of the second quarter of 2020. Additionally, in response to a reverse inquiry from a long-term strategic investor, this past Monday we re-opened portions of GE Industrial and GE Capital debt offerings, which were oversubscribed. This generated $3 billion in total additional proceeds, which we expect to use to reduce more of our shorter-duration debt, including repaying a portion of GE intercompany loan to GE Capital and repaying GE Capital’s future debt maturities.

We remain committed to our deleveraging goals of <2.5X Industrial net debt / EBITDA* and <4x Capital debt / equity—although we expect achieving them will take longer given the current environment. We are focused on keeping our financial position strong and safe with a keen eye on cash flow and capital discipline, leverage, and liquidity. Looking forward, we continue to monitor our operations in this environment, prioritizing maintaining a high level of cash and maximizing our flexibility as we evaluate any next steps.

__________________________________________________________________________________

6. Has COVID-19 slowed down the turnaround at Gas Power?

The Gas Power team continues to build on the turnaround progress that it made in 2019 and is accelerating additional cost and cash actions in order to further improve margins and free cash flow*.

Over the past 18 months, the Gas Power team has made considerable progress in improving the operations of the business including better underwriting standards, a renewed focus on project execution, fixed cost* out, and the implementation of lean. These actions resulted in better financial performance in 2019 and putting the business on better footing to deal with COVID-19, but there is more work to do.

As a result of COVID-19, we have seen some Gas Power customers deferring new equipment projects or delaying maintenance events to later in the year. These dynamics are our new reality and do present a challenge to near term growth and execution, but the team is adjusting accordingly by accelerating additional cost out and cash preservation actions that were planned for future periods to ensure continued operational and financial improvement. After reducing fixed costs* from $3.5B in 2018 to $3.1B in 2019, we now expect that Gas Power will reduce these costs to $2.5 billion in 2021. These accelerated actions combined with a focus on continuous operational improvement and the run-off of legacy inheritance cash items and projects will lead to high single digit margins and positive free cash flow* in Gas Power in 2021 with improvement thereafter.

__________________________________________________________________________________

7. Renewable Energy was supposed to be a primary turnaround focus in 2020. Is this still a priority and what are some of the signs that this business is turning?

The turnaround efforts at Renewable Energy continue to be a top priority for GE. The team is focused on strengthening its position in Onshore Wind, bringing the Haliade-X offshore wind turbine to market, and improving the cost structure and execution of Grid and Hydro.

Returning GE Renewable Energy to positive margins and free cash flow* over time is still a top priority for the company and is an important element of the company achieving high single digit free cash flow margins* over time.

To fully appreciate the efforts being put forth by the Renewables team, it’s helpful to describe the business in its various operating units. Our Onshore Wind business is experiencing strong growth supported by the U.S. Production Tax Credit (PTC), and the team is spending a significant amount of time improving project execution, controlling costs, and expanding services to make that growth profitable. On May 27, the United States Treasury Department issued new guidance granting an additional year of continuous effort to achieve commercial operation to PTC-eligible projects, which should create a larger market and/or better returns for developers. This is a strategically important business to GE and we expect to improve margins in line with our peers over time. Our Offshore Wind team is focused on the continued development and cost out of our Haliade-X wind turbine, which has seen significant customer interest as evidenced by the 5 gigawatts of commitments won in 2019. We expect Offshore to become a multi-billion dollar revenue product line by the mid-2020s. And our Grid and Hydro businesses are turnarounds where the team is continuing to improve deal underwriting, reduced fixed costs*, and run off legacy projects -- all under recently appointed new leadership.

Across the board, the Renewable Energy team is focused on taking cost out by continuous rationalization of its manufacturing footprint, labor productivity plans integrated with new manufacturing technologies (especially in blades), and the delayering of HQ structures with a shift in decision making to the operating units. Despite COVID-19 disruptions, the team has been able to complete large and complex wind farms across the world (most recently completed the installation of 123 onshore wind turbines at the Coopers Gap wind farm in Australia) and perform service maintenance remotely using smart-helmets connected with engineers at home. While not all of these efforts have resulted in better segment financial performance yet, we are starting to see real signs of progress on the ground in each business and expect those improvements to continue as the teams focus on fewer, more impactful priorities and embrace the lean culture that is taking hold across the company.

__________________________________________________________________________________

8. Excluding the impact of COVID-19, are you still targeting the same financial framework for Healthcare that you described at the December 2019 Radiological Society of Norther America (RSNA) conference?

While COVID-19 has increased the demand for some products used in the fight against COVID-19 and reduced demand for non-COVID related products, the team continues to target the mid-term financial targets that were described at the 2019 RSNA conference.

In Healthcare, we have been on the front lines of the battle against COVID-19 both in terms of delivering critical equipment to customers and ensuring that the existing installed base is serviced and available for utilization. While some of our product lines such as respiratory, CT, monitoring solutions, X-ray, anesthesia and point-of-care ultrasound have seen an increase in demand, other product lines have been pressured due to the deferral of certain procedures. As a result, we expect our 2nd quarter results to be sequentially worse with improvement in the second half of 2020.

Excluding what we are seeing for 2020, the near to mid-term financial targets that we described at the 2019 RSNA conference remain intact including low to mid single digit top line growth, 25-75 basis points of margin accretion per year, and free cash flow conversion* between 85% and 95%. At that time, we also shared our goals to reduce general & administrative costs as a percent of sales by 1.0 to 1.5 percentage points over the next several years off of a baseline of 8.7%. We have taken actions already this year to accelerate that progress and are expecting to deliver a 1 percentage point improvement on that ratio in 2020. We are also focused on efficiently accelerating and delivering NPIs by optimizing our existing product platforms to introduce new technology that our customers are looking for while keeping costs low.

As previously described, we are seeing some positive signs in the return of deferred procedures as evidenced by our weekly CT and MR scans data, we are accelerating the speed at which we take cost and cash actions such as headcount and reductions in capital expenditures, and we are rapidly deploying lean tools across our operations to improve working capital management. GE Healthcare remains at the center of Precision Healthcare, and we are confident in the long term growth, margin, and free cash flow* prospects of this business.

Top image: GE Aviation’s Riverworks aviation facility in Lynn, Massachusetts, has produced more than 1,600 of the F414 engines, which have collectively logged 4 million flight hours.

__________________________________________________________________________________

*Non-GAAP financial measure

CAUTION CONCERNING FORWARD-LOOKING STATEMENTS: This document contains "forward-looking statements" –that is, statements related to future events that by their nature address matters that are, to different degrees, uncertain. For details on the uncertainties that may cause our actual future results to be materially different than those expressed in our forward-looking statements, see http://www.ge.com/investor-relations/disclaimer-caution-concerning-forward-looking-statements as well as our annual report on Form 10-K and quarterly reports on Form 10-Q. We do not undertake to update our forward-looking statements. This document also includes certain forward-looking projected financial information that is based on internal estimates and forecasts. Actual results could differ materially.

NON-GAAP FINANCIAL MEASURES: In this document, we sometimes use information derived from consolidated financial data but not presented in our financial statements prepared in accordance with U.S. generally accepted accounting principles (GAAP). Certain of these data are considered “non-GAAP financial measures” under the U.S. Securities and Exchange Commission rules. These non-GAAP financial measures supplement our GAAP disclosures and should not be considered an alternative to the GAAP measure. The reasons we use these non-GAAP financial measures and the reconciliations to their most directly comparable GAAP financial measures are included in our annual report on Form 10-K and our quarterly reports on Form 10-Q, our 2020 GE Investor Outlook, and the GE 1st quarter 2020 earnings presentation, as applicable.

ADDITIONAL INFORMATION ABOUT GE: GE’s Investor Relations website at www.ge.com/investor and our corporate blog at www.gereports.com, as well as GE’s Facebook page and Twitter accounts, contain a significant amount of information about GE, including financial and other information for investors. GE encourages investors to visit these websites from time to time, as information is updated, and new information is posted.