Electrification Software Energy

Marco Annunziata: Oil Prices Got You Down?

The sharp decline in oil prices has placed them squarely at the center of the global economic debate. Many see low oil prices as evidence that the world economy has lost steam. Stock markets jump anxiously at every piece of news coming from the oil market.

The market story is important. But more important is that the oil and gas market is undergoing a deeper and more complex transformation, one that will have powerful repercussions over the coming decades.

The world needs more and more energy. And the energy industry must meet that growing demand in a period of higher uncertainty and volatility. That will require greater efficiency, adaptability and sustainability, which can be achieved in part through through the adoption of digital solutions.

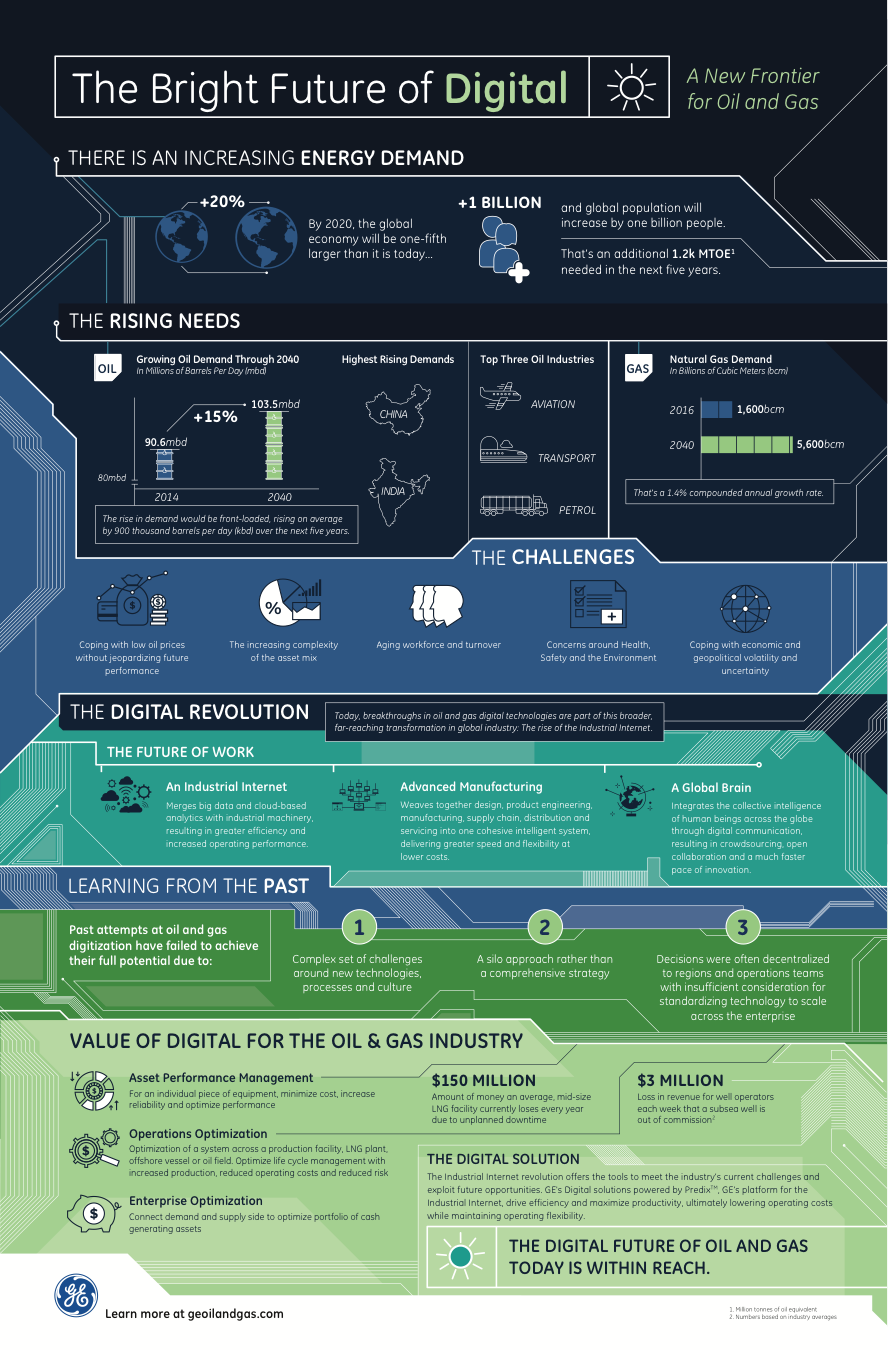

Energy Demand Heading in One Direction — Up

Even with the slowdown of China, global oil demand kept increasing at a robust pace through 2015. By September, it was 9 percent higher than at the peak before the Great Recession.

In the future, the need for energy will only grow. By 2020 the global economy will be one-fifth larger in real terms, and the global population will have increased by about 1 billion. By 2015, total primary energy demand will have increased by close to 15 percent, according to the International Energy Agency’s central scenario.

This increase in demand can only be met by leveraging all available energy sources. Today, oil accounts for about 30 percent of total energy demand; oil, gas and coal together for 80 percent. There are different views, and a lot of uncertainty, on how the energy mix will change in the coming decades. The most likely scenario is that the share of renewables will keep rising, and natural gas will experience fast growth. But oil will remain an important part of the equation.

The IMF projects that the world economy will keep growing at an annual pace of about 3.5 percent — in line with the pre-crisis average of 1980-2006. A larger part of this growth now takes place in emerging markets, which are more energy-intensive than advanced economies.

The bulk of global oil consumption (55 percent) is in the transport sector. Today, China has only seven cars per 100 inhabitants, and India only four. The U.S. has 82. China and India will take time to even partially fill the gap, and will impose more stringent pollution standards in the process — China is already moving in that direction. But even so, there is substantial pent-up demand for transportation that will be unleashed by economic growth. The same applies to aviation.

Don’t get me wrong, I am not trying to predict where oil prices will go. I am simply pointing out that we will still need a lot of oil and gas, together with all other energy sources.

An Uncertain Environment

Meanwhile, the oil and gas industry faces a number of challenges.

The most immediate challenge is copying with low prices without jeopardizing future performance. During the previous decade, the cost of projects ballooned, and oil-producing countries expanded public spending — most of them today need oil prices at $100 per barrel to balance their budgets. Governments now need to cut expenditures and diversify the economy. Oil and gas companies need to increase efficiency and productivity.

A second challenge comes from the increasing technical complexity of the asset mix. Oil and gas companies have developed far more complex facilities — e.g. unconventional fields, liquefied natural gas (LNG) and floating liquefied natural gas (FLNG) — that demand higher levels of engineering and operations expertise.

The third challenge is posed by the aging and turnover of the industry’s workforce: by some estimates, as much as 50 percent will have retired by 2025, taking decades of knowledge and experience with them. The industry does not have a comparable pipeline of younger workers to fill the gap.

Last but not least, the oil and gas industry needs to cope with a global environment characterized but much higher uncertainty and volatility, driven by technological innovations, economic developments, geopolitics and regulations. The industry will need to achieve a greater degree of flexibility and adaptability in order to cope.

A Digital Solution

Part of the solution will come from the faster adoption of digital solutions. In a recently released paper (LINK) we have detailed how Industrial Internet solutions can deliver value through three dimensions:

- Asset performance management: minimize cost, increase reliability, and optimize performance for an individual piece of equipment

- Operations optimization: system-wide improvements (e.g. across a production facility, LNG plant, offshore vessel or oil field), and optimized life cycle management with increased production, reduced operating costs and reduced risk

- Enterprise optimization: connection of demand and supply operations to optimize portfolio of cash-generating assets

Digital solutions can also help to preserve the accumulated knowledge and experience embodied in the outgoing workforce to transmit it to newer generations.

The adoption of these digital solutions should be part of a broader strategy. This will encompass targeted investments to increase efficiency and productivity; difficult choices on production capacity, especially on the higher cost sources like oil sands and deepwater; and renewed investment in human capital.

Today, low prices and fears on demand growth capture all the attention. But the true challenge will be to meet a growing demand for energy in a way that is efficient and sustainable from both a technical and environmental perspective — and to mitigate the cyclical swings in capex, production and prices that could otherwise cause substantial future shocks to the global economy.

Read more on the digital energy outlook in the white paper, Digital Future of Oil & Gas & Energy.

(Top image: Courtesy of GE)

Marco Annunziata is the Chief Economist and Executive Director of Global Market Insight at GE.

Marco Annunziata is the Chief Economist and Executive Director of Global Market Insight at GE.